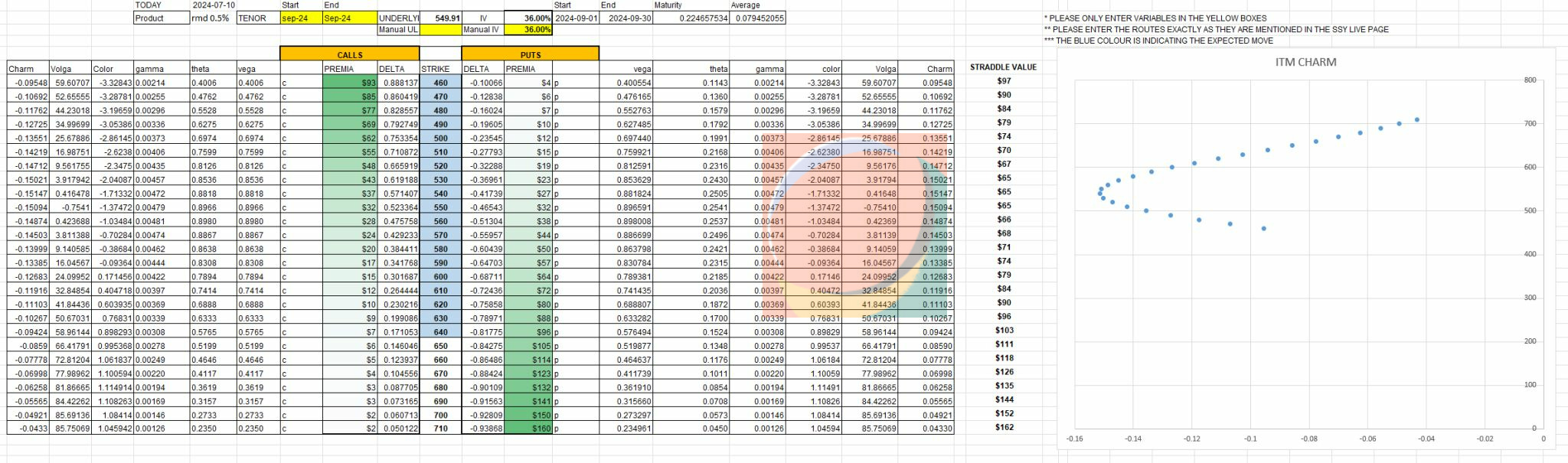

In the money Charm (of oil)

Understanding the charm of in-the-money (ITM) options for oil futures, such as Rotterdam barges 0.5%, requires a nuanced approach. Charm, also known as delta decay, plays a crucial role in options trading strategies, especially for commodities like oil.

Charm Dynamics for ITM Oil Options

ITM options for oil futures exhibit unique charm characteristics:

High Charm Magnitude: Similar to out-of-the-money (OTM) options, ITM options generally have higher charm values compared to at-the-money (ATM) options.

Directional Behavior: For ITM call options on oil futures, the charm is typically positive, indicating that delta increases as time passes. Conversely, ITM put options usually have negative charm.

Time Sensitivity: The charm effect intensifies as the option approaches expiration, becoming more pronounced in the final weeks before expiry.

Implications for Oil Options Trading

Understanding ITM charm for oil options can significantly impact trading strategies:

Risk Management

ITM options carry high directional risk due to their larger deltas. While their charm is strong, the rapid delta changes can lead to substantial price movements, requiring careful position management.

Hedging Considerations

Traders dealing with ITM oil options must be prepared to adjust their hedges more frequently, especially as expiration nears. The accelerating delta decay can quickly alter the overall portfolio risk profile.

Strategy Selection

For speculators, ITM positions in oil options are often less desirable despite their faster charm. The high directional risk outweighs the benefits of rapid delta decay for many traders.

Practical Applications

When trading ITM oil options:

Regular Monitoring: Keep a close eye on delta changes, especially over weekends when charm effects can accumulate.

Adjustment Thresholds: Consider setting specific delta thresholds for adjusting positions to manage the increasing directional exposure as the option moves deeper ITM.

Expiration Management: Be prepared to make more frequent adjustments or consider closing positions as expiration approaches to avoid unwanted exposure to physical oil delivery.

Conclusion

While ITM oil options exhibit strong charm characteristics, their high directional risk makes them challenging for speculative positions. Traders focusing on selling options may find more favorable risk-reward profiles in OTM options, where strong charm combines with lower directional risk. However, for those engaged in complex hedging strategies or market-making activities, understanding ITM charm remains crucial for effective risk management in the volatile oil futures market.