Backwardation Contango Definitions and Meaning

And why futures curves have no forecasting abilities

I often hear from market participants that X market is in Y condition thus underlying will go “insert direction”. Thus I think it is necessary to explain that most market participants are fully aware that future curves are far from perfect and most certainly do not indicate direction of any market, even if we are aware that is has mean reverting characteristics.

Forward vs. Future

The efficient market hypothesis suggests that the mean future spot price, or forward price, is simply the current spot price adjusted for the risk-free rate:

Fx=E(St)=ertS0Fx=E(St)=ertS0

Futures contracts allow market participants to exchange cash now for a specified asset at a future date. Essentially, the price of a futures contract reflects the present value of an asset—like a hamburger—set to be delivered on Tuesday.

In a frictionless market, these two prices would align perfectly. However, such ideal markets are rare; frictionless commodities remain a theoretical concept.

Market Dynamics

Commodity markets are not frictionless, meaning that while future prices can fluctuate, forward prices may remain stable.

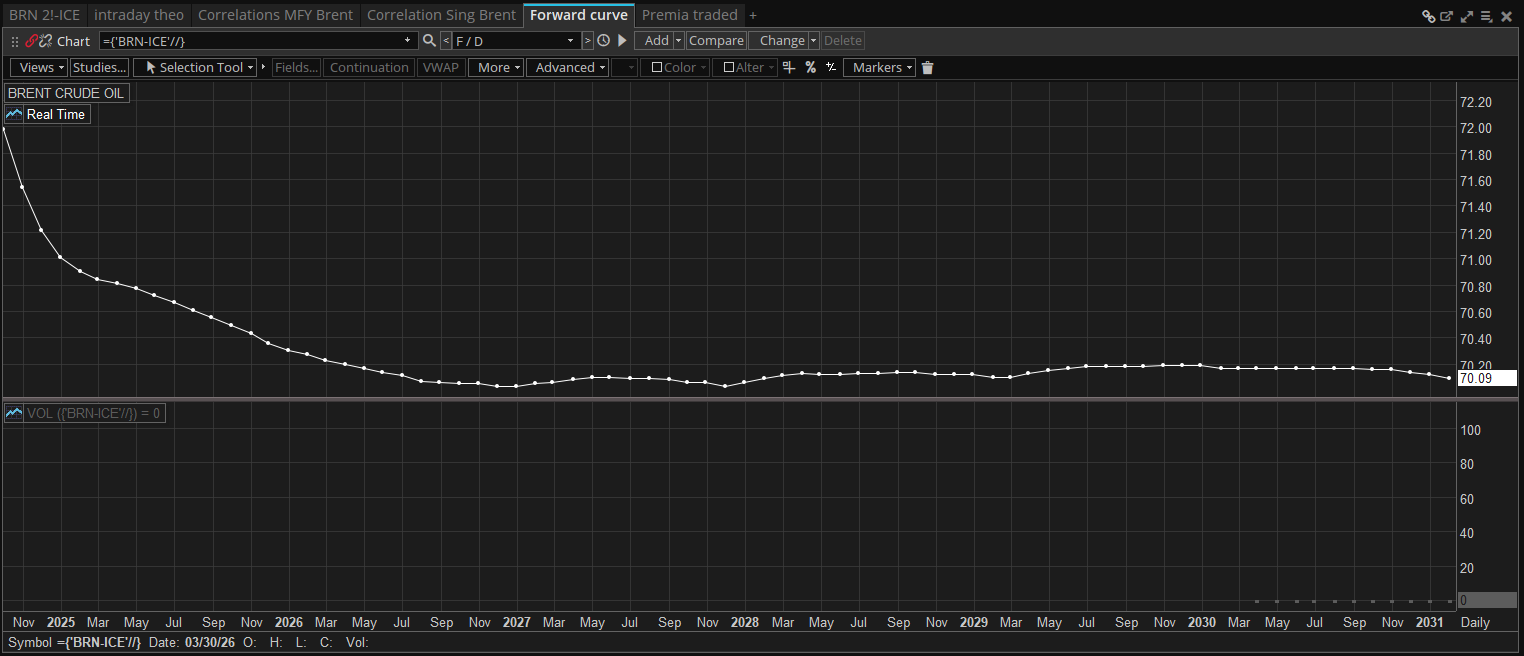

Contango

The term "contango" originated in 19th-century England and is believed to refer to a fee paid to defer payment when buying from a seller. When future prices exceed forward prices, the market is said to be in contango. This is typical for futures markets due to costs associated with carrying inventory, insurance, and other factors.

Once a commodity is delivered, the owner assumes responsibility for costs like storage fees and risks associated with physical assets. Additionally, cash today offers more flexibility than a futures contract, often leading to far-dated future prices trading at a discount compared to forward prices.

Backwardation

Conversely, backwardation occurs when a commodity is perceived as more valuable now than it will be in the future. For instance, agricultural products may be more plentiful post-harvest, or energy products may see reduced demand as spring approaches. In such cases, futures trade below the EMH-implied forward price. It's important to note that contango and backwardation should not be interpreted merely as directional indicators for commodity prices; doing so would contradict the efficient market hypothesis. While future and forward prices must converge at expiration, this can happen through various mechanisms.

Observing Market Trends

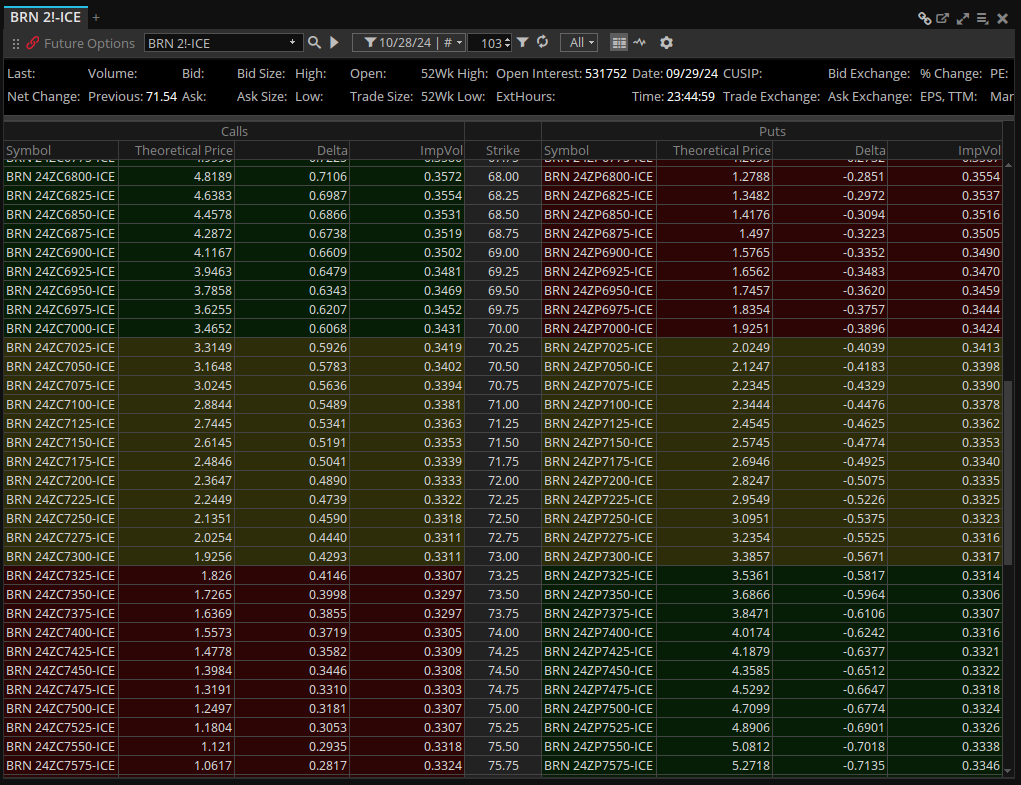

While analysing the futures curve can provide insights, implied volatility and liquidity tend to be more significant factors for retail traders and speculators.

Characteristics of Backwardated Markets:

Scarcity of the commodity

Low inventories

Price volatility due to low inventories

Strongly rising prices

A "fear" premium

Characteristics of Contango Markets:

Glut of the commodity

High levels of inventory

Relative price stability

General price weakness

A "complacency" discount

In sectors like crude oil and metals, backwardation is often observed due to supply shortages or surges in demand. Conversely, precious metals typically experience contango due to their abundant availability above ground and relatively low storage costs. Crude oil storage is expensive—approximately 20% of a barrel's cost—which discourages holding onto it. Understanding these dynamics can help traders navigate the complexities of commodity markets more effectively.

I like this. The backwardation long trade is one that keep an eye out for.